Complaints Procedures

When a bank client has a complaint about a bank product or service, there are a number of ways to “complain”.

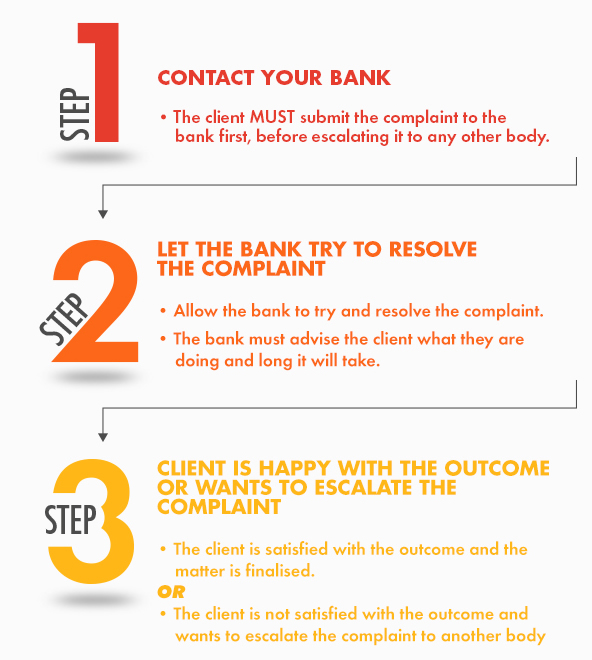

The Banking Association introduced a specific dispute resolution policy in 2003 that is binding on all its member banks. This policy prescribes the process and other requirements when a bank receives and manages a complaint from a client. There are a number of steps a client must follow in the complaint process – let’s see what they are:

If you are not satisfied with the outcome of a complaint lodged with your bank, you can do the following:

DOWNLOAD FULL ACT

Please note that is only as a brief summary of the main provision of the Code and should not be relied upon as a legal document. There are many other provisions and exemptions under the Code. For more detailed information and the full Code please download the Code of Banking Practice.

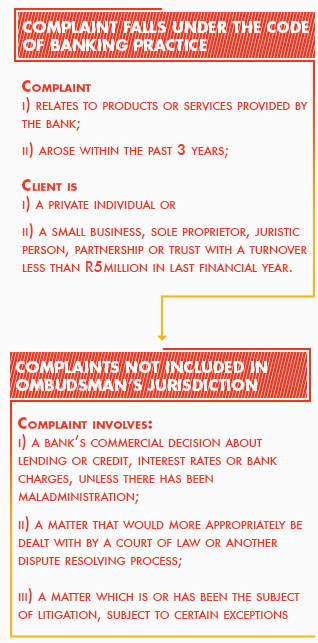

The Code of Banking Practice applies to all retail products and services of a bank provided to individuals and certain small legal entities. All banks which are members of The Banking Association subscribe to the Code and are therefore bound by the obligations and undertakings.

OMBUDSMAN FOR BANKING SERVICES

The Ombudsman for Banking Services scheme (the OBS) was established under the Financial Services Ombud Schemes Act, No. 37 of 2004. The Ombudsman for Banking Services provides individual and small business bank customers with a free, fair, quick and effective dispute resolution process. The Ombudsman for Banking Services resolves matters by investigating complaints lodged against banks, in accordance with OBS rules, and provided the Ombudsman for Banking Services has jurisdiction. Unresolved matters after investigation and negotiation may be subject to a formal decision by the OBS. The decision may be in the form of a determination that is binding on the bank or is a commendation that is not.

A complainant is free to seek alternative remedies such as instituting legal proceedings or other dispute resolution processes, at any time while the matter is under investigation, provided the complainant informs The Ombudsman’s Office so that they can close the file.

Your complaint must conform to the following to be considered by the OBS:

Relates to products or services provided by the bank;

Involves a claim of R2m or less;

Arose within the past 3 years;

The bank concerned is a member of The Banking Association.

Complaints that fall outside The Ombudsman for Banking Services include:

Commercial decisions taken by banks regarding lending or credit, interest rates or bank charges, unless maladministration has occurred; As such The Ombudsman’s Office cannot assist you in getting the bank to approve credit or alter your terms of repayment on a loan.

Matters that would be dealt with more appropriately by a court of law or another dispute resolution process;

Matters that are or have been the subject of litigation, subject to certain exceptions.

The Ombudsman’s role in the financial industry is to investigate complaints by members of the public, to mediate between the parties to the dispute, and, where the mediation is not successful, to make recommendations for the settlement of the complaints.

Reana Steyn is National Financial Ombud Scheme (NFO) .

Visit the National Financial Ombud Scheme

DOWNLOAD FULL ACT

Please note that is only as a brief summary of the main provision of the Code and should not be relied upon as a legal document. There are many other provisions and exemptions under the Code. For more detailed information and the full Code please download the Code of Banking Practice.

When the complaint relates to a product which falls under FAIS, it can also be referred to the FAIS Ombudsman – but not to both The Ombudsman for Banking Services and the FAIS Ombudsman.

FAIS OMBUDSMAN

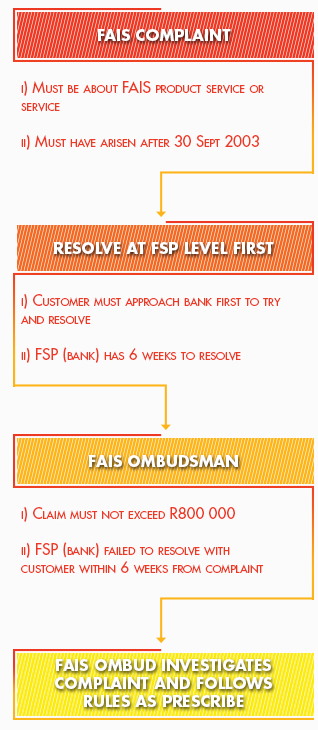

The Office of the Ombud for Financial Services Providers (‘FAIS Ombud’) was established by the Financial Advisory and Intermediary Services Act, No 37 of 2002 (‘FAIS Act’). Consumers of financial products have the right to complain about any inappropriate advice given or service rendered in relation to a particular financial product. The FAIS Ombud’s role is to resolve disputes between financial services providers and their clients in a fair, informal, quick and effective manner.

A complaint must conform to the following in order to be considered by the FAIS Ombudsman:

It must fall within the jurisdiction of FAIS.

It must have arisen at the time that FAIS was effective i.e. on or after 30 September 2004.

The complaints procedures required by FAIS are aligned with The Banking Association complaints procedures.

In addition, a complaint must conform to the following in order to be considered by the FAIS Ombud:

The claim must not exceed R800,000.

The Financial Services Provider (FSP) must have failed to address the complaint satisfactorily within 6 weeks.

The FAIS complaint may not be the subject of pending or current litigation.

The FAIS Ombudsman is Mr Charles Pillay

Website: www.faisombud.co.za

DOWNLOAD FULL ACT

Please note that is only as a brief summary of the main provision of the Code and should not be relied upon as a legal document. There are many other provisions and exemptions under the Code. For more detailed information and the full Code please download the Code of Banking Practice.

When the complaint relates to a product which falls under the NCA, it can be referred as described below, but generally the complaint will be referred to the Ombudsman for Banking Services or the FAIS Ombudsman before any other action is taken.

NCA

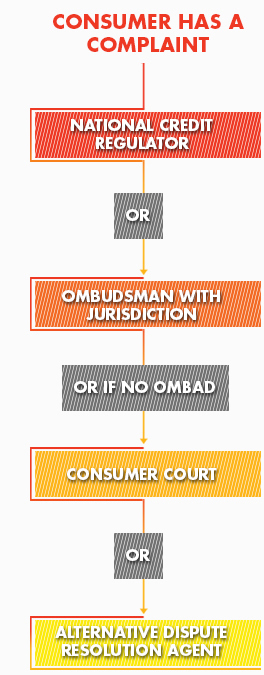

- The NCA introduces various channels to lodge complaints (Section 134):

- To the National Credit Regulator (NCR).

- To the National Consumer Tribunal.

- To a Consumer Court.

- To an Alternative Dispute Resolution Agent.However:The NCR will refer a complaint back to the credit provider (bank) if the consumer has not tried to resolve it at that level first.The National Consumer Tribunal will also require that the matter must first be dealt with by the consumer and the credit provider (except in certain instances, e.g. when the NCR lodges a complaint directly to the National Consumer Tribunal – [Section 141]).Therefore:

- NCA related complaints in relation to banks must:

- Be addressed between the complainant and the bank first;

- Then referred to the Ombudsman for Banking services or the FAIS Ombudsman;

- Even if lodged at the NCR – it will be referred to the relevant Ombudsman by the NCR.

- The National Credit Regulator is Mr Gabriel Davel

Website: www.ncr.org.za

DOWNLOAD FULL ACT

Please note that is only as a brief summary of the main provision of the Code and should not be relied upon as a legal document. There are many other provisions and exemptions under the Code. For more detailed information and the full Code please download the Code of Banking Practice.