News

Loan Pricing From a Commercial Bank

Publication Date: 29/01/2020

By Pierre Venter

Banks contribute positively to society by enabling simple, safe and efficient management of money.

Banks are profit-orientated businesses which strive to provide both investors and shareholders alike with a reasonable return on their money. The vast majority of the loans which they provide to customers are financed by depositors’ money.

They therefore strive to balance the risk they incur on lending these monies as they have a fiduciary responsibility to safeguard a depositor’s funds. For a bank to attract investors and shareholders to place their money with them, so that this money can in turn be lent out to customers, banks are required to pay these investors a return on their investment and depositors’ interest on their deposits. This is referred to as the cost of funding.

Banks are also required to cover the cost of maintaining the infrastructure (such as computer systems, premises and staff) required to enable a bank to fulfill its role as a bank, and to fulfill every transaction or deal required by its customers.

The cost of funding as well as infrastructure costs are collectively known as the hurdle rate. Each product house is required to achieve the hurdle rate in order for a bank’s treasury department (which manages a bank’s assets and liabilities) to allocate finite capital to it, for lending to customers.

This short document aims to explain, in general terms, how banks determine an interest rate for a loan – including a mortgage loan.

OVERVIEW OF INPUTS TAKEN INTO CONSIDERATION WHEN DETERMINING AN INTEREST RATE

Below are key inputs that considered when determining an interest rate:

• The term of the Loan

• The loan amount

• The probability that the customer will default – termed probability of default (PD)

• Once the customer defaults, the loss that the bank will incur on the loan – termed loss given default (LGD)

• Cost of funding the loan

• Capital required and the cost of holding such capital (banks are required to retain sufficient capital to meet depositor requests for the repayment of their deposits

• Any income expected to be received over the term of the loan

• Interest income

• Any other income (such as fees)

• Any expenses expected over the term of the loan.

HOW DOES A BANK MODEL?

In order to remain viable and to attract depositor and shareholder funds, a bank has a hurdle rate requirement that it needs to achieve, termed its return on equity. A model is used to establish the hurdle rate required for a portfolio of loans.

The model only considers the projected income and expenditure over the entire loan term. In other words, the cost versus the profit of the loan to the bank. The other factors of the loan, such as the capital and the loan amount determine the income and expenses of the loan to the bank.

The interest rate is the only factor which can be altered to get to the hurdle rate requirement. The model therefore keeps all other factors besides the interest rate constant (this means the loan amount and term can’t be changed), with the interest rate varying in order to achieve the hurdle rate.

LOAN AMOUNT AND TERM

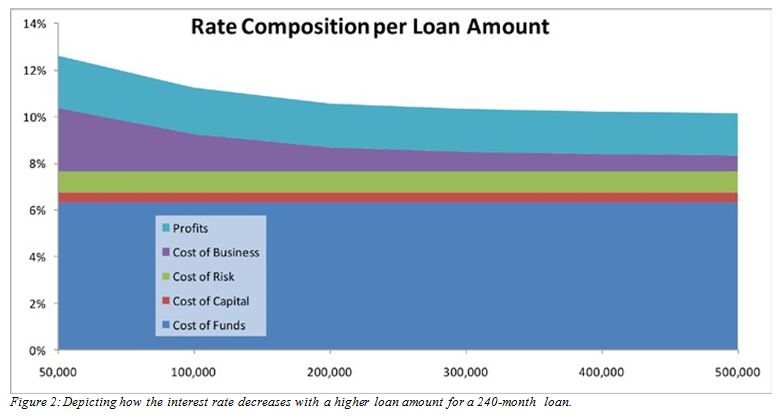

Generally, the bigger the loan amount and the longer the loan term, the lower the interest rate will be. This is because:

• The nett interest rate income received is higher on larger loans as compared to smaller ones, for example 1% on R100 000 is R1 000 per annum and 1% on R 1 000 000 is R10 000 per annum;

• The time required for a bank to cover all its fixed costs and thus achieve the desired return is greater for longer term loans.

Expenses are not necessarily directly proportional to the balance of the loan. Only the Cost of Funds and Cost of Capital would be, everything else stays constant. For example, the cost of approving and placing a loan on a bank’s books is say R4 000 per loan, and thereafter the cost of maintaining a loan on a bank’s books is say R40 per month. These costs reflect a fixed cost for a bank, irrespective of the loan amount.

Generally, the interest income generated from a R500 000 loan will be more compared to a R100 000 loan. It follows that a bank will still be able to recover its costs if it offers a lower interest rate on bigger loans.

Consider Figure 2 (page 33) which is a depiction of how the interest rate decreases with a higher loan amount for a 240-month loan.

PROBABILITY OF DEFAULT (PD)

Banks use predictive models that are mostly based on the customer’s historical credit behaviour, in order to assess a customer’s propensity to repay the advanced loan diligently, or for the customer to default in repayment (assuming that affordability at inception is in order).

These probabilities vary across products, with unsecured products generally reflecting riskier business than secured loans, as banks can recover a portion of the debt for secured loans from the security offered by the customer in support of the loan (for example, a mortgage bond).

LOSS GIVEN DEFAULT (LGD)

Once a client has defaulted, a lender calculates the loss that it expects to incur as a percentage of the balance at the point of default. In the case of a mortgage loan, the loss incurred is the final write-off amount after the property was repossessed and a legal sale in execution was done, or the property was voluntarily sold.

LGD is therefore based on the actual property, whereas PD focuses on the probability of the client repaying the loan.

Table 1: An example of calculating loss

| Balance at the point of Default | R400 000 |

| Value realised at the auction | R250 000 |

| Less Credit Loss Cover | R70 000 |

| WRITE-OFF | R80 000 |

Based on the example in Table 1, a bank expects to lose R80 000 from a R400 000 balance, which is a 20% LGD (R400 000 divided by R80 000).

In the above example, loan cover (the credit loss cover), reduces the LGD by 17.5 %. Even though customers pay for the credit loss cover, they receive a better interest rate than a loan without this, as the LDG is lower. Such cover enables banks to increase their risk appetite and still be able to offer a more affordable interest rate.

QUICK EXPECTED LOSS CALCULATION EXAMPLE

The client defaults with a balance of R400 000. The Client’s PD was 5% (over 12 Months) and the expected LGD through previous experience is 20%. Thus, the expected loss is R400 000 x 5% x 20%, which is R4 000. Therefore, when modelling, a bank will need to account for the fact that for this deal they may lose R4 000. All deals are modelled on an individual basis and such a loss will depend on the PD and LGD for that specific client or deal.

Pricing is therefore done on the basis that the interest income stream is adjusted so that the hurdle rate is achieved, whilst taking the expected loss into account. Figure 3, below, shows the effect of PD and LGD on expected loss and hence the interest rate that is charged to a borrower.

COST OF FUNDS

As discussed earlier in this paper, the Cost of Funds is the biggest expense when considering a loan or a mortgage loan.

Cost of Funds generally follows the Bank Repo Rate, as published by the South African Reserve Bank (SARB). If a lender cannot attract sufficient deposits or investments to cover the loans it makes, then the SARB is the lender of last resort for lenders. If a bank is sufficiently capitalised, it will cover its loans from deposits or investments held from the public, the cost of which is normally slightly lower than the SARB Repo Rate.

COST OF CAPITAL

The Banks Act, 1990 and Amendments/Regulations thereto, require banks to hold capital on each loan, which is a predefined percentage depending on risk factors and a bank’s ability to match the term of deposits or loans.

Capital holding is sloped in such a way that the higher the PD and LGD, the more capital that is required to be held. Thus, the higher the cost of capital, the higher the interest rate quoted to a customer for the bank to make its required return (hurdle rate).

OTHER INCOME

Apart from interest income, which forms the majority of the income stream, banks may charge an initiation fee on a loan, as well as a monthly service fee, and potentially any insurance commissions earned. Such fee income formulas or ceilings are prescribed within the National Credit Act, 34 of 2005. The thinking behind an initiation fee is to offset the costs of setting up the loan, including the valuation fee, to cover the cost of valuing the property, and the monthly service fee is to offset the ongoing cost of managing such a loan.

EXAMPLE

Analysing a loan of R400 000, a PD of 5% and an LGD of 20% over a 48-month breakeven period. This means that loans are priced such that a breakeven point of the required return on equity is achieved in 48 months. This would therefore indicate that loans are most likely not profitable prior to this period.

Table 2: Bank profit over 48-month breakeven period.

| INCOME | R144 250 |

| Interest (@ 10.2%) | R139 300 |

| Initiation Fee | R3 500 |

| Annual fee | R1 450 |

| EXPENSES | R120 274 |

| Cost of Funds (@ 6.34%) | R86 390 |

| Cost of Capital | R5 797 |

| Account Set up Costs | R12 670 |

| Account Maintenance | R2 631 |

| Bad Debt Provision | R12 786 |

| FINAL PROFIT | R23 976 |

Table 2 above, shows that after 48 months; the bank realises a profit of R23 976. This is based on a return to capital of 20% per annum.

Looking at this a different way, the bank makes a profit of 1.7% of the average loan balance in the 48-month period after the figure is annualised. The split below shows the composition of the interest rate and is based on average balance.

Table 3: Composition of interest rate based on average balance.

| Interest Rate | 10.2% |

| Cost of Funds | 6.34% |

| Cost of Capital | 0.42% |

| Cost of Risk | 0.92% |

| Business Costs | 0.7% |

| Profits | 1.7% |

CONCLUSION

The Home Loan business for a bank is a volatile business, as it is dependent on economic cycles and long-term investor confidence in a country. By its very nature, property is a commodity which operates within a cyclical bubble which ranges from bust to boom. Whilst it compares favourably with other forms of asset classes over the long term, there are risks which both lenders and consumers alike face, especially when property prices are in the decline due to tough economic conditions, a stock over supply, or economic or political uncertainty.

Housing is also a socio-economic need for families; one should view property not only from an investment perspective, but also from a family perspective. It has an economic growth and job creation effect on the economy. Whilst it can be viewed as the backbone for wealth creation, it also carries with it social and political sensitivity, which makes the role of a responsible lender that much more important.

WHAT IS INTEREST AND AN INTEREST RATE?

• Interest is a fee the bank charges for lending people money.

• This fee is based on something called an interest rate.

• Interest rates are generally determined by the repo rate and the South African Reserve Bank has the mandate to set the repo rate.

• The repo rate is the rate that the Reserve Bank charges commercial banks.

• The Reserve Bank’s mandate is to ensure sustainable economic growth and price stability for the South African economy. assessment.

WHAT INTEREST RATE OPTIONS MAY BE AVAILABLE TO ME AS A CUSTOMER?

• Getting a preferential rate is dependent on the customer’s individual risk profile and credit record.

• To arrive at the individual rate, the bank is required to perform an affordability assessment before granting credit as required by the National Credit Act.

• The National Credit Act also regulates the maximum interest rates that commercial banks may charge customers.

• For Home Loans, banks will look at a number of factors when assessing the customer’s application for a home loan, including:

• Income

• Actual expenses

• Credit Profile or Credit Record

• Current credit exposure (how much debt you currently have or are owing to creditors)

• The term of the loan

• Amount of loan being applied for

• The property to be mortgaged

• Whether you have a deposit or not

THE CHALLENGE OF AFFORDABILITY

• Whilst credit records, conduct of accounts and actual monthly budgets play a key role when assessing home loan applications, affordability accounts for the largest portion of customers’ home loan applications being declined.

• In cases where applicants have healthy credit records and good financial conduct, some simply cannot afford the monthly instalment based on their actual living expenses as measured using a detailed affordability assessment.

• Banks’ affordability assessments are in line with the requirements of the National Credit Act, 2007, as amended.

• The NCA has significantly changed the approval landscape, rightly so to protect both customers and the banks from the effects of reckless lending.

• So, the simplistic repayment-to-income measurement has evolved to a more realistic understanding of a customer’s actual financial circumstances.

Pierre Venter is the general manager, Human Settlements in Market Conduct Division at the Banking Association South Africa.